Now Reading

AllianceBernstein: What You Didn’t Know About European Offices

AllianceBernstein: What You Didn’t Know About European Offices

Published 07-17-24

Submitted by AllianceBernstein

Clark Coffee| Chief Investment Officer and Head—European Commercial Real Estate Debt

Are European offices broken? We don’t think so. They’re just different.

Make no mistake: office properties face challenges on both sides of the Atlantic, including higher-for-longer interest rates and lower valuations that, in some cases, will create refinancing challenges. But we believe certain factors make European offices less volatile than those in the US.

This doesn’t mean now is the time to focus on office space. In fact, we think the opportunity set is more attractive in other commercial real estate sectors. But we expect demand for the right type of European office property to remain high, and investors who understand the differences between Europe and the US may have a better chance of tapping Europe’s potential in the future.

Office Supply: Europe May Have Less

So, what is it that makes Europe different?

Let’s start with supply. Remote and hybrid work arrangements have had far-reaching effects on the value and utility of office space everywhere. European gateway cities, however, tend to have less office stock per capita than US ones. This may be because most cities in Europe lack US-style “midtowns” and the glass office towers that dot so many US skylines (the La Défense financial and business district of Paris is an exception).

That’s an important distinction, because when those towers become obsolete, they’re notoriously difficult to convert into residential housing. Many are inflexible super-structures that come with environmentally unfriendly systems and floor plates that can’t easily or cost-effectively be adapted to suit tenant needs. Carving them into dwellings with plumbing and access to natural light is a challenge.

Based on our analysis of office space per capita, the US is the world’s most oversupplied office market, with considerably more space than major European markets, including the UK, France and Germany.

What’s more, the oversupply in many US gateway cities is dominated by outdated space that’s poorly suited to what employers and employees want out of offices today: aesthetically pleasing, environmentally friendly designs, with proximity to transit and open spaces that promote collaborative work environments.

Footprints Matter, Too

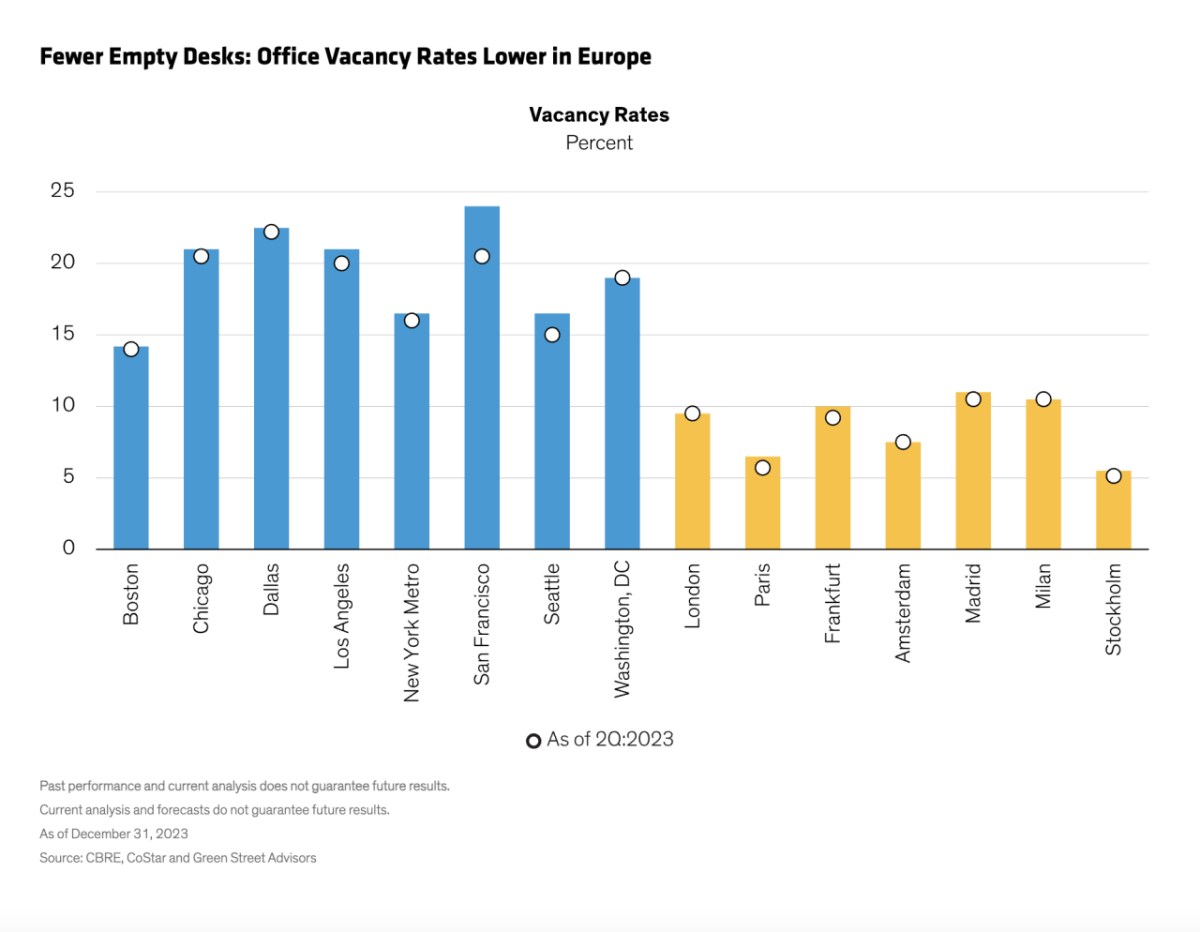

Europe may score better on supply issues because the smaller, narrower footprints of European buildings can be easier to repurpose. Between 2015 and 2022, for example, more than 73,000 residential units were created in the UK through the repurposing of outdated office stock, according to Savills, a global real estate services provider. This may help explain why office vacancy rates, which rose everywhere during the pandemic, are lower in major European cities (Display).

Change of Scenery: More Demand for Time in Office

There are differences on the demand side of the equation, too, that we think may shed more light on Europe’s lower vacancy rates in office space.

First, European homes tend to be smaller across most income levels, leaving little space for a home office. According to one study, homes in France, Germany, the Netherlands and the Nordic countries average two to three rooms per household member, compared with nearly four in the US.

Then there’s the comfort level of working remotely. European city dwellers are less likely to have air conditioning, so some may find working in an office more comfortable during the summer. In winter, the lack of double-glazed windows can make home offices too chilly.

European commute times are typically shorter, too. The reverse is increasingly true in the US, where drives to work are getting longer. Economists at Stanford University recently found that morning commutes between 50 and 74 miles rose 18% in the US between 2019 and 2024. Commutes of more than 75 miles rose by 32%. Some participants in the study said they could tolerate the longer commutes because hybrid work arrangements meant they only had to make them once or twice a week.

Greener Requirements Are Transforming Workspaces

European regulators are also influencing office supply and demand dynamics simply by requiring landlords to implement minimum energy performance standards before they can lease properties. As we see it, this does two things: it drives investment that will “future-proof” these properties while at the same time accelerating the obsolescence of properties that don’t make the grade.

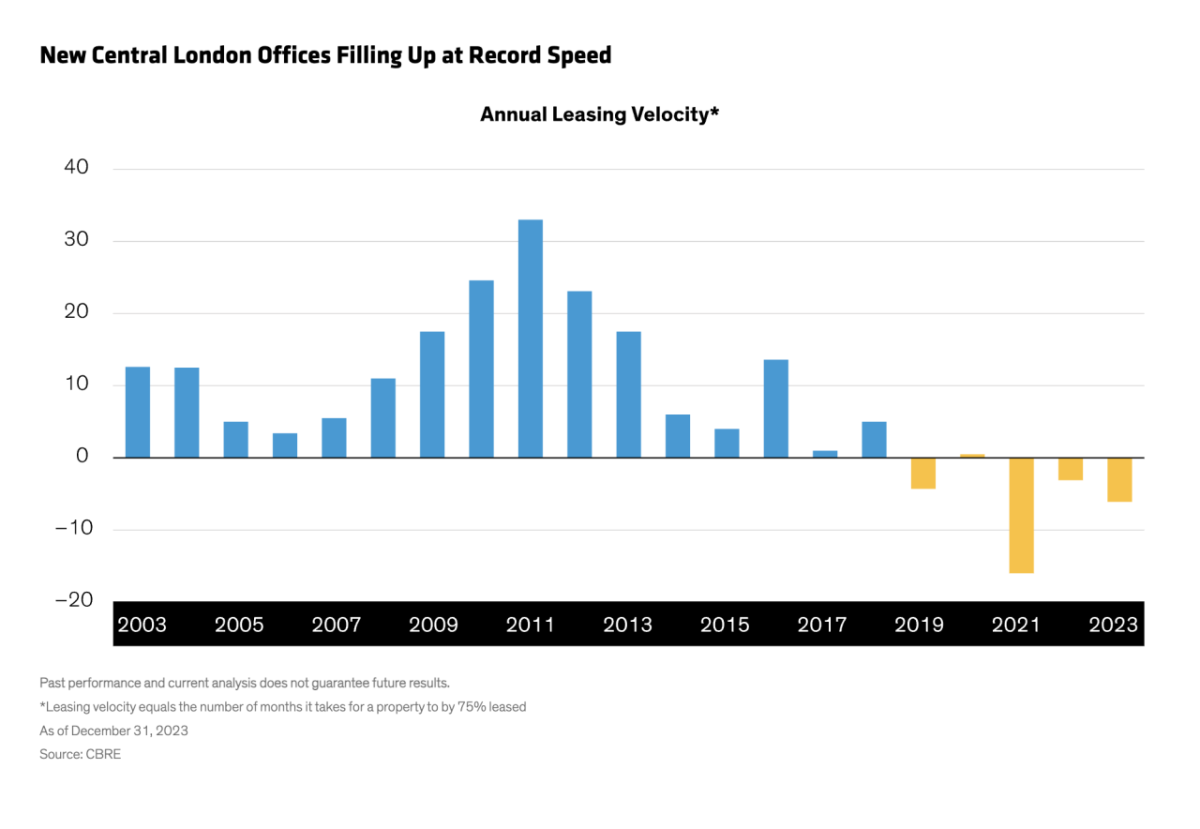

Leasing for “next generation” office space in London, for example, is near a 15-year high. This suggests that demand tends to be high for properties that tick the right boxes, which is visible in the declining length of time it takes them to reach a 75% leasing threshold (Display). In recent years, buildings have been 75% pre-leased (indicated by the negative bars) in an average of five months prior to completion.

We think this helps explain why prime office rents grew by an average of 4.9% across major European cities between the third quarter of 2022 and the third quarter of 2023.

Demand for “next generation” buildings is high in US cities, too, and we expect it to create opportunities for investors. But there’s a wrinkle: the US lacks a uniform federal mandate for environmental, social and governance (ESG) reporting, which can complicate development and leasing decisions. Opposition to ESG considerations in some areas of the country may also slow the process.

Don’t get us wrong: investors need to tread carefully when it comes to Europe’s office sector. For now, we think the most attractive commercial real estate investments can be found elsewhere. But those who avoid painting Europe and the US with the same brush may find it easier to capitalize on opportunities as they arise.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

About the Author

Clark Coffee is the Chief Investment Officer and Head of European Commercial Real Estate Debt. His previous business, Lacarne Capital, was acquired by AB in 2020 to establish the firm’s real estate debt business in Europe. Previously, Coffee was head of Tyndaris Real Estate, where he was responsible for building the business into a top-10 real estate debt fund in Europe. Prior to that, he co-headed origination for Deutsche Bank’s European commercial real estate credit business and oversaw the risk management and restructuring of more than €2 billion of troubled loans during the global financial crisis. Coffee holds a BA in economics from Lake Forest College and an MBA from the University of Michigan. Location: London/Frankfurt

Learn more about AB’s approach to responsibility here.

AllianceBernstein

AllianceBernstein

AllianceBernstein (AB) is a leading global investment management firm that offers diversified investment services to institutional investors, individuals, and private wealth clients in major world markets.

To be effective stewards of our clients’ assets, we strive to invest responsibly—assessing, engaging on and integrating material issues, including environmental, social and governance (ESG) considerations into most of our actively managed strategies (approximately 79% of AB’s actively managed assets under management as of December 31, 2024).

Our purpose—to pursue insight that unlocks opportunity—describes the ethos of our firm. Because we are an active investment manager, differentiated insights drive our ability to design innovative investment solutions and help our clients achieve their investment goals. We became a signatory to the Principles for Responsible Investment (PRI) in 2011. This began our journey to formalize our approach to identifying responsible ways to unlock opportunities for our clients through integrating material ESG factors throughout most of our actively managed equity and fixed-income client accounts, funds and strategies. Material ESG factors are important elements in forming insights and in presenting potential risks and opportunities that can affect the performance of the companies and issuers that we invest in and the portfolios that we build. AB also engages issuers when it believes the engagement is in the best financial interest of its clients.

Our values illustrate the behaviors and actions that create our strong culture and enable us to meet our clients' needs. Each value inspires us to be better:

- Invest in One Another: At AB, there’s no “one size fits all” and no mold to break. We celebrate idiosyncrasy and make sure everyone’s voice is heard. We seek and include talented people with diverse skills, abilities and backgrounds, who expand our thinking. A mosaic of perspectives makes us stronger, helping us to nurture enduring relationships and build actionable solutions.

- Strive for Distinctive Knowledge: Intellectual curiosity is in our DNA. We embrace challenging problems and ask tough questions. We don’t settle for easy answers when we seek to understand the world around us—and that’s what makes us better investors and partners to our colleagues and clients. We are independent thinkers who go where the research and data take us. And knowing more isn’t the end of the journey, it’s the start of a deeper conversation.

- Speak with Courage and Conviction: Collegial debate yields conviction, so we challenge one another to think differently. Working together enables us to see all sides of an issue. We stand firmly behind our ideas, and we recognize that the world is dynamic. To keep pace with an ever changing world and industry, we constantly reassess our views and share them with intellectual honesty. Above all, we strive to seek and speak truth to our colleagues, clients and others as a trusted voice of reason.

- Act with Integrity—Always: Although our firm is comprised of multiple businesses, disciplines and individuals, we’re united by our commitment to be strong stewards for our people and our clients. Our fiduciary duty and an ethical mind-set are fundamental to the decisions we make.

As of December 31, 2024, AB had $792B in assets under management, $555B of which were ESG-integrated. Additional information about AB may be found on our website, www.alliancebernstein.com.

Learn more about AB’s approach to responsibility here.

More from AllianceBernstein