Now Reading

Learning the Language of Sustainability Planning and Climate Reporting

Learning the Language of Sustainability Planning and Climate Reporting

Published 04-27-23

Submitted by NRG Energy

Originally published on NRG Energy Insights

Now more than ever, organizations are prioritizing sustainability planning to achieve long-term climate goals. However, not every business has a dedicated team. In many cases, leaders take on such planning as an added responsibility outside of their traditional job scope.

Like many fields, sustainability has its own language with a long list of terms related to environmental, social, and governance (ESG) factors. Being able to understand and speak the language is key to pursuing, tracking, and reporting sustainability outcomes. Here, we focus on terms in one of the most critical areas: climate.

For energy and facility managers helping to lead their companies’ sustainability efforts, these terms are essential to ensure their businesses can set appropriate climate goals, and then track and report progress using best-practice standards.

Climate vocabulary basics

Climate-related sustainability action is needed because of the impact of greenhouse gas emissions that magnify both climate change and human-induced global warming. These factors are the foundation, so it’s important to have a firm grasp of what those three highlighted terms mean.

- Greenhouse gases (GHGs) are a set of naturally occurring or human-generated gases that transform the atmosphere. According to Cornell Law School, humans generate most GHGs through actions such as agriculture and burning fossil fuels for energy, manufacturing, and transportation purposes. GHGs include carbon dioxide (CO2), methane (CH4), nitrous oxides (NxO), and manufactured fluorinated gases.

- According to NASA, climate change is a long-term change in the average weather patterns that have come to define Earth’s local, regional, and global climates. Changes observed in Earth’s climate since the mid-20th century have been driven by human activities that have increased heat-trapping GHG levels in Earth’s atmosphere, raising Earth’s average surface temperature. While natural processes also contribute to a changing climate, they are far outpaced by human-induced activities.

- NASA defines global warming as the long-term heating of Earth’s surface observed since the post-industrial period due to human activities that increase GHG levels in Earth’s atmosphere. This term is not interchangeable with the term climate change but rather is a key component of a changing climate.

Climate disclosures

At face value, climate disclosures are not complicated at all. They are simply any disclosure your company makes about the impact of its operations on climate change, such as GHG emissions totals, use of renewable energy, or energy savings from energy efficiency efforts.

However, climate disclosures get complicated when the topic of standards and requirements is introduced. In the United States, the Securities and Exchange Commission (SEC) in March 2022 proposed rules to enhance and standardize climate-related disclosures for investors. If finalized, investor-owned companies subject to SEC regulation will be required to make certain climate-related disclosures, including information about climate-related risks.

These disclosures are reasonably likely to have a material impact on their business, results of operations, or financial condition, and certain climate-related financial statement metrics within their audited financial statements.

Beyond the SEC rules, which won’t apply to all businesses, there are other voluntary standards for climate disclosures. For example, the Task Force on Climate-related Financial Disclosures or TCFD, created by the Financial Stability Board, has issued recommendations on climate disclosures supported by more than 3,000 companies across 92 countries. The nonprofit CDP runs a widely accepted global disclosure system to help companies manage their environmental impacts.

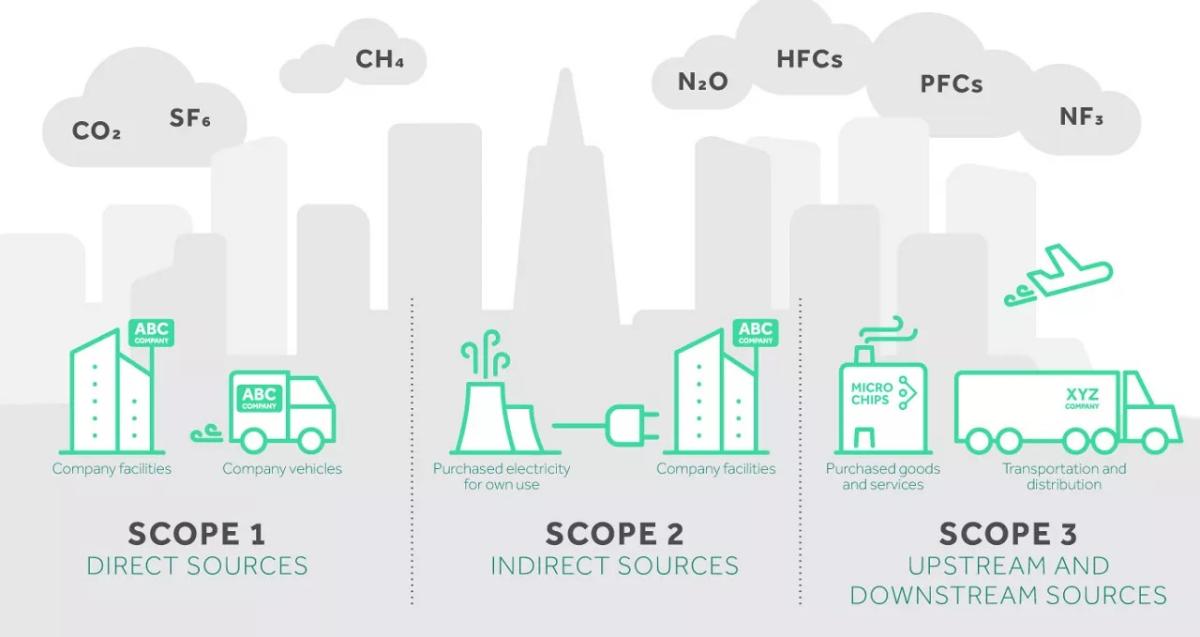

Scope 1, 2, and 3 Greenhouse Gas Emissions

Many businesses include GHG reduction goals in their sustainability plans, which means they need to track GHG emissions and disclose annual GHG emissions from operations to show progress toward their goals.

Simple, right? Not so fast. Who’s responsible for the GHGs created by the Amazon and FedEx trucks that deliver your products to customers? What about GHGs from the electricity delivered by your local electric provider to keep your business running?

The Environmental Protection Agency (EPA) provides helpful definitions for different categories — or “scopes” — of emissions so that businesses can track and report GHGs and GHG reductions consistently.

Scope 1

Direct GHG emissions that occur from sources that are controlled or owned by an organization (e.g., emissions associated with fuel combustion in boilers, furnaces, company-owned fleet vehicles).

Scope 2

Indirect GHG emissions associated with the purchase of electricity, steam, heat, or cooling. Although an organization’s Scope 2 emissions physically occur at the facility where they are generated, they are accounted for in the organization’s GHG inventory because they are a result of the organization’s energy use.

Scope 3

Indirect GHG emissions resulting from activities not owned or controlled by an organization, but that the organization indirectly impacts in its value chain. Scope 3 emissions for one organization are the Scope 1 or 2 emissions of another organization and often represent the majority of an organization’s total GHG emissions.

Any company with a GHG reduction goal will be expected to track and report Scope 1 and 2 emissions, while Scope 3 emissions may be considered optional. The Greenhouse Gas Protocol, a global nonprofit, has developed a widely accepted corporate accounting and reporting standard with guidance for companies preparing a GHG inventory.

Net-zero emissions

The World Economic Forum defines net-zero emissions as “a state of balance between emissions and emissions reductions.” For an individual business to reach net-zero, that does not mean it cannot emit any GHG emissions from operations. It means the business must offset its Scope 1, 2, and 3 emissions through verified means of reducing other GHGs, such as through the purchase of renewable energy credits or carbon offset credits, carbon capture, sequestration, and/or other technologies.

As with GHG reporting, there is an internationally recognized standard for achieving net-zero, also called carbon neutrality.

Net-zero is becoming a rallying point for businesses across the globe. More than 1,200 companies have committed to science-based net-zero targets. Being a sustainable business is one of five pillars of NRG, and we are proudly committed to our own climate targets. As an organization, we set an ambitious goal to achieve net-zero and reduce our carbon footprint by 50% by 2025, using our 2014 emissions as our base year.

Science-based Target-setting

Did you notice the term “science-based” in the last paragraph about net-zero targets? Many companies have been criticized for greenwashing by claiming carbon neutrality with the use of various trading and accounting measures, while their operations still produce significant real emissions. According to the Science Based Targets initiative (SBTi), emissions targets are considered “science-based” if they are in line with what the latest climate science deems necessary to meet the goals of the United Nations Paris Agreement — limiting global warming to 1.5°C above preindustrial levels.

SBTi is a partnership of the United Nations, CDP, World Resources Institute (WRI), and others that defines and promotes best practices in emissions reductions in line with climate science. Nearly 1,000 organizations have set emissions reduction targets grounded in climate science through the SBTi’s guidance.

Get started

We all have a role to play in creating a more sustainable future through planning and action. When it comes to climate and energy, look for a trusted advisor who can help you implement a range of solutions to track, report, and ultimately achieve your sustainability goals.

NRG Energy

NRG Energy

At NRG, we’re bringing the power of energy to people and organizations by putting customers at the center of everything we do. We generate electricity and provide energy solutions and natural gas to millions of customers through our diverse portfolio of retail brands. A Fortune 500 company, operating in the United States and Canada, NRG delivers innovative solutions while advocating for competitive energy markets and customer choice, working towards a sustainable energy future.

More from NRG Energy