Now Reading

Leveraging Mobile Money To Drive Financial Inclusion of Women

Leveraging Mobile Money To Drive Financial Inclusion of Women

Published 04-12-23

Submitted by Ericsson

In many countries, mobile money services have become an alternative to traditional banking systems. Data from Global Findex and FinScope studies show that in at least 20 low- and middle-income countries more women have a mobile money account than a bank account. In 10 of these 20 countries, the leading mobile money service is powered by the Ericsson Wallet Platform. In this special blogpost on International Women’s Day, we will discuss the importance of financial inclusion of women and how mobile money advances equity and equality for women, breaking down barriers which have in the past hampered female progression in developing nations.

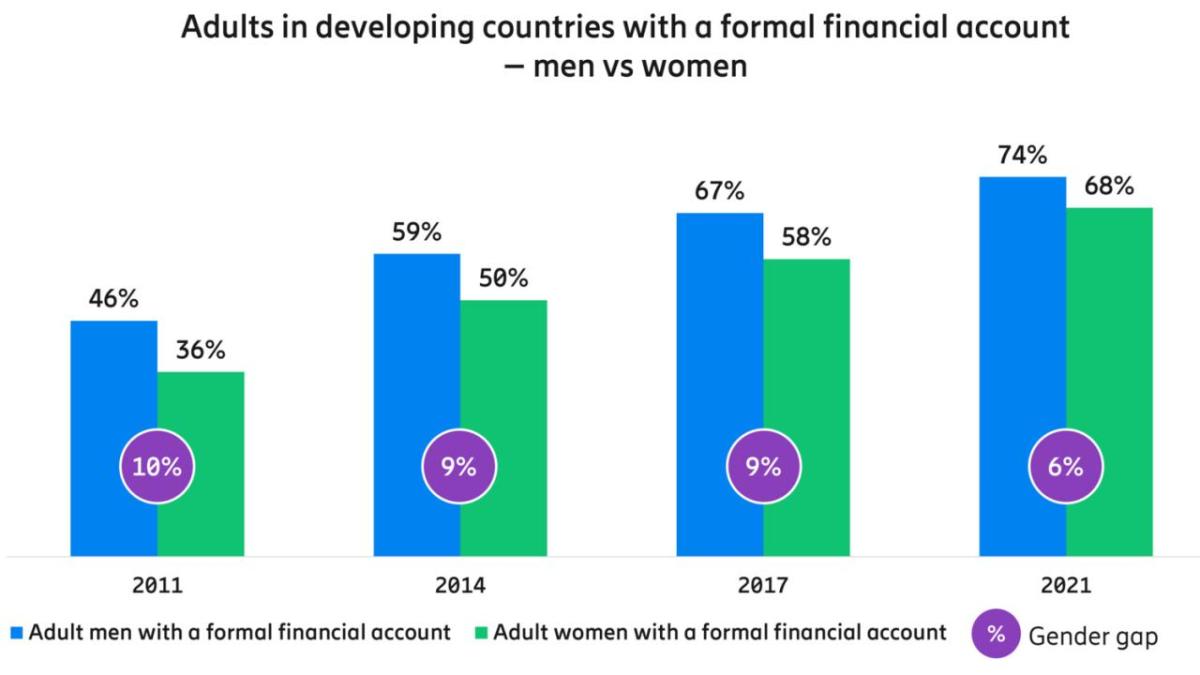

The World Bank’s Global Findex Database 2021 shows that the world has made considerable progress towards female financial inclusion in the last 10 years. The gender gap in formal financial account ownership across developing countries has fallen from 9% to 6%, highlighting that women are getting closer to financial equality. Growth in account ownership by women is much faster than men and 68% of adult women in developing countries are now included in formal financial systems. In many developing countries, this growth in account ownership amongst women is mainly driven by mobile money.

Financial inclusion of women is critical for economic empowerment and society

In many cultures, women face gender bias while using financial services. Women are dependent on men to top-up their mobile connections, pay children’s school fees, and with purchasing household equipment. Due to social constraints, it can be difficult for women to go out to pay utility bills get loans to meet an emergency need, or support their entrepreneurial ambitions. Mobile money breaks the bias and brings parity between men and women in the access and use of financial services.

If women have a formal financial account, government and non-government organizations (NGOs) can directly transfer money and subsidies of welfare schemes to women’s accounts instead of to a male member of the family. Crediting money or subsidies directly to women’s accounts eliminates intermediaries, reduces leakages due to corruption, removes duplicate beneficiaries and accelerates the pace of welfare programs. More importantly, this enables financial independence of women, allowing them greater control over their funds and spending money on essential needs like education, their family, and savings.

A study from Niger on monetary-aid distribution primarily to women after a drought found that social benefits paid directly into mobile money accounts instead of cash offered women greater privacy and control over their funds and boosted spending on nutritious food. Household diet diversity was 9% to 16% higher amongst households who received mobile money transfers and children ate 1/3 more of a meal per day. These results can be partially attributed to time savings associated with mobile money transfers, as recipients spent less time traveling to and waiting for their transfer. Moreover, the operational cost of mobile money transfers was 20% less than cash payments.

The Global Findex Report 2021 also suggests that low-cost formal savings accounts help women to improve their financial health, save on a more regular basis, and shift their spending to relevant household needs such as buying nutritious food, reducing their reliance on debt, and preparedness for financial emergencies.

Mobile money drives financial inclusion for women

Complex account opening processes and requirements of multiple documents prevent many women from opening a bank account, which means that women in developing countries are generally excluded from banking systems. Furthermore, opening fees, maintenance fees, and minimum balance requirements mean that many women can’t afford to maintain the regular costs associated with a bank account. Banks also have a limited number of branches and due to social restrictions, women are unable to travel long distances to access their accounts.

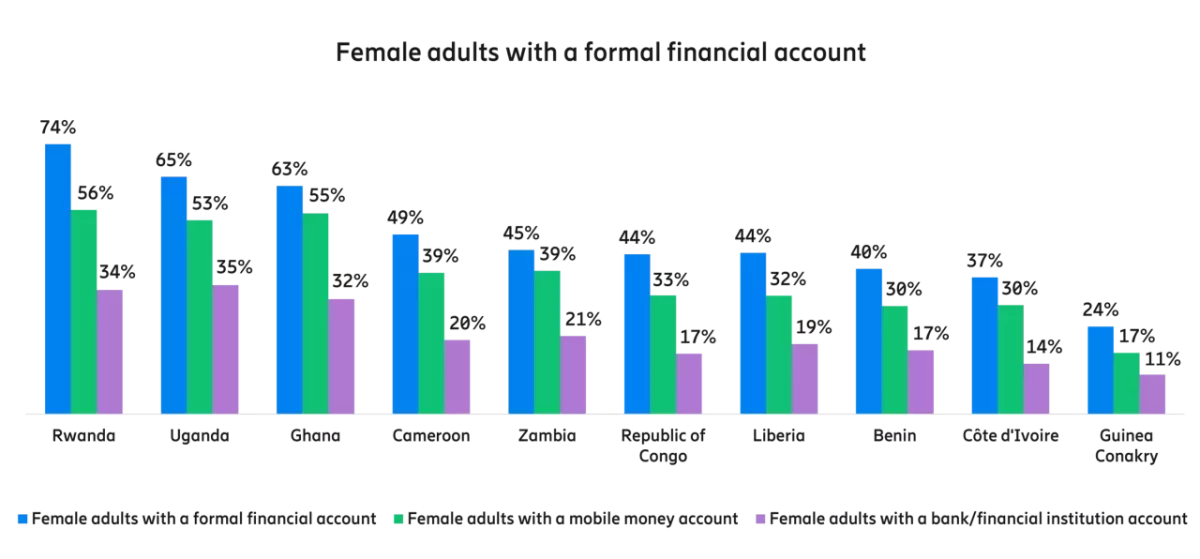

By comparison, mobile money accounts have a simple registration process which requires less documentation and better affordability with zero fees and no minimum balance requirements. Consequently, in many developing countries mobile money services have become a leading alternative to banking systems. Data from Global Findex and FinScope studies corroborates this with reports showing that in at least 20 low- and middle-income countries more women have mobile money accounts than bank accounts. In 10 of these 20 countries the leading mobile money service is powered by Ericsson Wallet Platform, our global fintech platform. In three of these countries, Rwanda, Uganda, and Ghana, more than half of the adult female population has a mobile money account. Furthermore, in six of 10 countries, 30% to 40% of the female adult population has a mobile money account.

Unsurprisingly, in most of these countries less than 20% of the female adult population has a bank account. The numbers indicate that in these countries mobile money has contributed substantially to increasing the financial inclusion of women.

Mobile money helps to narrow the gender gap of financial access in some countries. For example, in Liberia the gender gap in mobile money account ownership is 8 percentage points, compared to bank or financial accounts where it is 19 percentage points. In Uganda, Ghana, Cameroon, and Liberia, more women than men have only a mobile money account. For example, in Ghana 31% women have only a mobile money account compared to 27% of men.

Service providers encourage the adoption of mobile money amongst women by offering services focused on women. Examples include grant distribution for girls’ education into their mother’s mobile money account, insurance and monetary support for healthcare, subsidy disbursement to women for shifting to clean cooking fuels, micro-loans for women entrepreneurs running small and medium-sized businesses, and many more. Mobile money also digitizes traditional financial tools mainly used by women like savings clubs, burial societies, village savings and loans associations (VSLAs) making them more secure, transparent, and easy-to-use. In some countries, female merchants make up a considerable part of local markets. Mobile money enables these low-income merchants to go digital, accept mobile payments, and modernize their businesses at low-cost.

United Nation’s Sustainable Development Goal 5 (SDG 5) promotes gender equality. Mobile money is an important tool in achieving one of the SDG 5 targets of giving women equal rights to access and use of financial services.

Addressing the barriers hampering financial

Inclusion of women

The trend towards female equity and equality is encouraging, but more needs to be done to close the financial gender gap. For this, we have listed four main challenges and suggested ways to address them:

1.Lack of documentation

Problem: A prominent barrier in financial inclusion is the lack of identity (national ID) and other documents needed to open a financial account. In Sub-Saharan Africa, 37% of adults cite the lack of documents as a reason for not having financial account.

Solution: Mobile money lowers this barrier as it requires less documentations than banks. Moreover, regulators and mobile money providers should adopt a flexible or tiered Know Your Customer (KYC) approach with no KYC, partial KYC and full KYC options to open mobile money account. A woman without any documentation can register with a no KYC option but will get limited services and lower transaction limits. Whereas, the woman providing all documents can be registered for the full KYC account having access to all services and higher transaction limits. For women without documents in areas like rural, tribal, or refugee settlements, regulators should permit alternative documents like letters from a village head, a beneficiary ID, or a refugee certificate.

2.Lack of money

Problem: The most cited barrier to financial inclusion is the lack of money. Another barrier reported mostly by women is that another family member already has an account, so they don’t believe they need their own account. However, women should be educated that a financial account is not only for savings but is also very useful in emergencies to receive money and grants.

Solution: To encourage women to open a financial account, governments should design female welfare programs focused on paying grants and subsidies directly into their account. Mobile money accounts are most suitable and affordable to be the first formal financial accounts for women as they do not require any minimum balance, account opening fees, or maintenance fees. Women can keep their mobile money account active even with a zero balance.

| Destination | Kigali City | Southern Province | Western Province | Northern Province | Eastern Province | National Average |

| Umurenge sacco | 21:25 | 45:38 | 43:55 | 41:47 | 43:42 | 38:86 |

| MFI'S | 22:74 | 48:68 | 47:18 | 47:01 | 47:96 | 41:16 |

| Bank branch | 22:78 | 50:20 | 49:03 | 48:06 | 48:25 | 42:85 |

| ATM | 22:06 | 49:23 | 48:68 | 49:86 | 47:67 | 41:21 |

| Mobile money agent | 8:96 | 23:63 | 23:76 | 22:36 | 17:49 | 18:78 |

Source: FinScope Rwanda 2020

3.The travel distance to financial institutions

Problem: Most often, the distance to banks or ATMs is too far for women to travel. Distance is a barrier for 31% of unbanked adults in developing economies.

Solution: Mobile money providers have established extensive agent networks, multiple times bigger than bank and ATM networks. Mobile money agents offer registration, deposit, withdrawal, and over the counter payment services, bringing these last-mile services closer to consumers’ homes and overcoming the distance hurdle. For example, in Rwanda the average time to reach a mobile money agent is 18 minutes 78 seconds, while it is over 40 minutes for banks and other financial institutions.

4.Lack of a mobile phone

Problem:Compared to men, more financially excluded women do not have a mobile phone due to reasons such as high cost, social norms, etc. However, most mobile money services are available on inexpensive feature phones through the USSD interface, putting mobile money in reach of women at the bottom of the economic pyramid. The focus should be on reducing this digital divide and providing mobile phones to more women.

Solution:To lower the mobile phone cost barrier, telecom operators and mobile money providers should introduce device financing or pay-as-you-go device schemes that can help women to buy mobile phones in installments. Governments and non-governmental organizations should work on providing refurbished phones to underprivileged women, to enhance the digital and financial inclusion of women.

In addition to overcoming the above barriers, there are a few other steps required to increase the mobile money adoption of women:

- All stakeholders including governments, NGOs, regulators, industry bodies and mobile money providers should work collectively to roll out digital and financial literacy programs for women and create more awareness about the benefits and use of mobile money services.

- Raise the participation of women in the entire mobile money ecosystem. Mobile money providers should increase the proportion of female mobile money agents, enable more female merchants to accept mobile money, feature women in mobile money marketing campaigns and have more female employees at all levels of mobile money organizations from technology to leadership roles. This will create a more female-focused and female-friendly environment and generate more trust and comfort amongst women consumers.

- Governments and mobile money providers should enable a collection of more detailed gender-disaggregated data. A high quality of gender-disaggregated data can be a very useful tool to develop baseline targets, policies and programs to reduce the gender gap in financial inclusion.

It is encouraging to see that mobile money enables equal access to financial services and works towards increasing the financial inclusion of woman in many countries. However, this is just the beginning, and we need to increase the efforts multifold to fully close the gender gap in financial access. Ericsson Wallet Platform along with the mobile financial services it powers, will continue focusing on leveraging and enhancing mobile money as a tool to drive full financial inclusion for women.

References: World Bank’s Global Findex Database 2021 and FinScope Rwanda 2020

Visit Ericsson Mobile Financial Services page for more blogs, case studies and other content

Ericsson

Ericsson

Ericsson is one of the leading providers of Information and Communication Technology (ICT) to service providers. We enable the full value of connectivity by creating game-changing technology and services that are easy to use, adopt, and scale, making our customers successful in a fully connected world.

Our comprehensive portfolio ranges across Networks, Digital Services, Managed Services and Emerging Business; powered by 5G and IoT platforms.

More from Ericsson