Now Reading

How Green Bonds Will Fund a Green Future

By Tiffanie Wong CFA, Salima Lamdouar, and Patrick O'Connell CFA

How Green Bonds Will Fund a Green Future

By Tiffanie Wong CFA, Salima Lamdouar, and Patrick O'Connell CFA

Published 03-23-22

Submitted by AllianceBernstein

More securities labeled as environmental, social and governance (ESG) bonds are being issued by a wider variety of companies than ever before. This is a welcome development, because such financing will play a critical role in the global transition to a greener world. But not all ESG-labeled bonds are equal. To fund a genuinely green future, investors will need to separate the grain from the chaff.

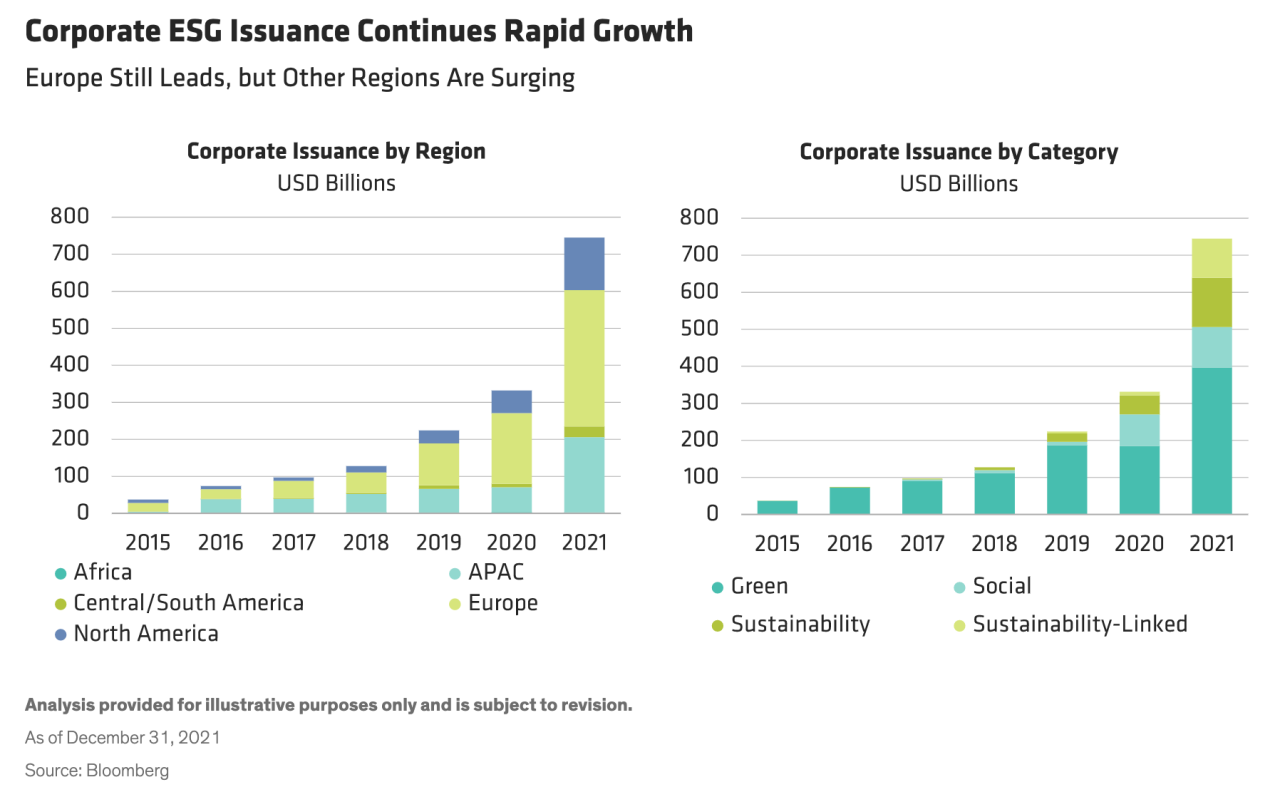

An Explosion of ESG Bond Issuance

ESG-labeled bond issuance surged to new heights in 2021. Though Europe remained the leader, new regions rapidly adopted these financing structures. Green bonds, which fund particular projects, continued to dominate. But issuance of social, sustainability and sustainability-linked bonds—which reference specific key performance indicators, or KPIs—grew fastest (Display).

The range of issuers has broadened as well. Until recently, ESG bond issuance was mainly the preserve of investment-grade issuers. But in 2021, high-yield issuance across US dollar and euro markets quadrupled. What’s more, many industries featured in the list of ESG bond issuers for the first time: in euro markets, chemicals, consumer products, and metals and mining; and in the US, autos, chemical and telecoms. The use of proceeds and range of projects widened too.

Further Strong Growth Expected for ESG Bonds

Can the rapid growth of ESG-labeled bond issuance continue? We believe it will, for three reasons. First, ESG factors are now affecting the cost of capital, with an increasing number of investors adopting strong ESG guidelines. Second, ESG has become a strategic priority for businesses. Natural language processing analysis of publicly available earnings call transcripts and conference presentations tells us that ESG is one of the hottest topics in corporate boardrooms—alongside input-cost inflation, supply chain problems and labor shortages. That’s hardly surprising because, third, companies are facing increasing investor scrutiny about their sustainability goals and continuous pressure to raise their game.

As a result, a raft of industries has committed to ambitious targets for future change. For instance, the steel sector plans to deploy 20 commercial-scale green steel facilities by 2030, marking a breakthrough on the path to net-zero emissions by 2050; 40 major cement and concrete producers committed to cut emissions by 25% by 2030 and to be net zero by 2050; and 80 aviation businesses and large corporate customers now aim to boost their green fuel usage to 10% of global jet fuel demand by 2030—a 1,000-fold increase from today, saving 60 million tons of CO2 per year and providing 300,000 green jobs.

Ambitious goals demand new capital, making them well-suited for ESG debt financing—and pointing toward continued rapid growth of the ESG-labeled bond market.

Investors Must Be Choosy About ESG-Labeled Issues

As new ESG-linked issues proliferate, it’s critical that investors use a disciplined framework to evaluate them. We believe that bonds whose terms merely gesture toward environmental and social factors but have no real impact are less likely to perform well over the long term—making a bond’s design as important as its price.

The first test bond investors must apply is materiality. Is the use of proceeds for a green bond significant to the issuer’s business and industry? Does the KPI target for a sustainability-linked bond represent a material improvement for the entire firm? We’ve noted instances where use of proceeds or KPIs covered only tiny parts of a company. By contrast, Faurecia’s Green Notes issue was fully aligned with the firm’s core mission of sustainable mobility, and its use of proceeds supports the company’s ambition to diversify into hydrogen-powered transport.

Green bond issuers should also provide a green bond framework or corporate plan, together with basic firmwide commitments, such as adopting a transition pathway in line with 1.5 degrees warming or aiming for net-zero carbon output on most relevant scopes (for most industries, that includes scope 3). Certain sectors, such as automakers and utilities, have their own specific climate undertakings—for example, a timeline for transitioning to all-electric vehicles. On the social side, look for policies that mitigate modern slavery risk.

Sustainability-linked structures that lack ambitious objectives are generally unattractive. Some KPI targets are overly generic and disappointingly modest. In these cases, investors need to press for specific goals and stretch KPIs, such as Henkel’s, whose KPIs are specific, set readily measurable goals across the whole business, include scope 3 emissions and feature some timelines as short as five years. Industry peer comparisons can help determine whether an issue’s terms can be benchmarked to best practices and whether KPIs are sufficiently demanding.

It’s also important to consider both the timeline of the KPIs and the penalty for non-performance. Issuers that fail to hit their KPI targets must typically pay an increased coupon to defray potential bond price losses from the negative ESG outcome. But investors need to scrutinize whether the coupon step-up adequately compensates for the miss, and whether they will receive enough enhanced coupon payments before the KPI timeline expires. Too many structures currently feature limited step-ups with back-ended penalties. If investors want a genuinely green future, they must push back against easy structures and limited repercussions.

Engagement Is Key

Bond issuers regularly need fresh injections of capital. By engaging with companies and bankers on ESG matters and bond structures, investors can be clear about the type of objectives and KPI targets they believe reflect best practice. Even if a company fails to set acceptable terms with a current bond issue, a continuing engagement program can secure better terms in future.

We believe that green and other ESG-labeled bonds will play a hugely important part in creating a green future. It’s up to investors to ensure that it arrives on time.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

About the Authors

Tiffanie Wong, CFA

Tiffanie Wong is a Senior Vice President and Director of Fixed Income Responsible Investing Portfolio Management. In this role, she is part of the leadership team that develops responsible investment strategy across AB's Fixed Income business, particularly related to integrating environmental, social and governance considerations throughout the team's portfolio construction processes and overseeing management of several of the team's sustainable strategies. Wong also serves as Director of US Investment-Grade Credit, responsible for the management and strategy implementation of the firm's US Investment-Grade Credit portfolios, including total-return and income-oriented credit strategies for institutional and retail clients. She has worked closely with AB's Quantitative Research team to leverage the firm's technology innovations within fixed-income trading and research to apply a more systematic approach to AB's credit investing. Prior to joining AB's Fixed Income portfolio-management team, Wong served as an associate portfolio manager on the Credit team, focusing on various strategies for the Global and US Credit portfolios-including total return, buy and hold, and liability matching. Before joining AB in 2012, she was a fixed-income portfolio analyst and trader at Segall Bryant & Hamill and a fixed-income portfolio associate at Wells Capital Management. Wong holds a BA in economics with a minor in business institutions from Northwestern University and is a CFA charterholder. Location: New York

Salima Lamdouar

Salima Lamdouar is a Vice President and Portfolio Manager for Sustainable Fixed Income, focusing on sustainable thematic credit, income and emerging-market debt strategies. Before joining the firm in 2015, she was a generalist portfolio manager at fixed-income manager Rogge Global Partners. Lamdouar holds a BSc (Hons) in banking and international finance from Cass Business School. Location: London

Patrick O'Connell, CFA

Patrick O'Connell is a Senior Vice President and Director of Fixed Income Responsible Investing Research. In this role, he is part of the leadership team that develops responsible investment strategy across AB's Fixed Income business, particularly related to integrating environmental, social and governance considerations throughout the team's research and engagement. Previously, O'Connell served as a corporate credit research analyst, focusing on emerging-market corporates in Latin American and African countries. He joined the Emerging Markets research team in 2013 after working as a credit analyst covering US high-yield energy credits at AB. Prior to joining the firm in 2012, O'Connell was a desk analyst at UBS Investment Bank, where he helped to allocate capital on the trading desk. He holds a BS in accounting and finance (magna cum laude) from Villanova University and is a CFA charterholder. Location: New York

AllianceBernstein

AllianceBernstein

AllianceBernstein (AB) is a leading global investment management firm that offers diversified investment services to institutional investors, individuals, and private wealth clients in major world markets.

To be effective stewards of our clients’ assets, we strive to invest responsibly—assessing, engaging on and integrating material issues, including environmental, social and governance (ESG) considerations into most of our actively managed strategies (approximately 79% of AB’s actively managed assets under management as of December 31, 2024).

Our purpose—to pursue insight that unlocks opportunity—describes the ethos of our firm. Because we are an active investment manager, differentiated insights drive our ability to design innovative investment solutions and help our clients achieve their investment goals. We became a signatory to the Principles for Responsible Investment (PRI) in 2011. This began our journey to formalize our approach to identifying responsible ways to unlock opportunities for our clients through integrating material ESG factors throughout most of our actively managed equity and fixed-income client accounts, funds and strategies. Material ESG factors are important elements in forming insights and in presenting potential risks and opportunities that can affect the performance of the companies and issuers that we invest in and the portfolios that we build. AB also engages issuers when it believes the engagement is in the best financial interest of its clients.

Our values illustrate the behaviors and actions that create our strong culture and enable us to meet our clients' needs. Each value inspires us to be better:

- Invest in One Another: At AB, there’s no “one size fits all” and no mold to break. We celebrate idiosyncrasy and make sure everyone’s voice is heard. We seek and include talented people with diverse skills, abilities and backgrounds, who expand our thinking. A mosaic of perspectives makes us stronger, helping us to nurture enduring relationships and build actionable solutions.

- Strive for Distinctive Knowledge: Intellectual curiosity is in our DNA. We embrace challenging problems and ask tough questions. We don’t settle for easy answers when we seek to understand the world around us—and that’s what makes us better investors and partners to our colleagues and clients. We are independent thinkers who go where the research and data take us. And knowing more isn’t the end of the journey, it’s the start of a deeper conversation.

- Speak with Courage and Conviction: Collegial debate yields conviction, so we challenge one another to think differently. Working together enables us to see all sides of an issue. We stand firmly behind our ideas, and we recognize that the world is dynamic. To keep pace with an ever changing world and industry, we constantly reassess our views and share them with intellectual honesty. Above all, we strive to seek and speak truth to our colleagues, clients and others as a trusted voice of reason.

- Act with Integrity—Always: Although our firm is comprised of multiple businesses, disciplines and individuals, we’re united by our commitment to be strong stewards for our people and our clients. Our fiduciary duty and an ethical mind-set are fundamental to the decisions we make.

As of December 31, 2024, AB had $792B in assets under management, $555B of which were ESG-integrated. Additional information about AB may be found on our website, www.alliancebernstein.com.

Learn more about AB’s approach to responsibility here.

More from AllianceBernstein